2,73%

2,73%EU Trade Agreements and Stainless Steel: Between Market Openness and Strategic Safeguards

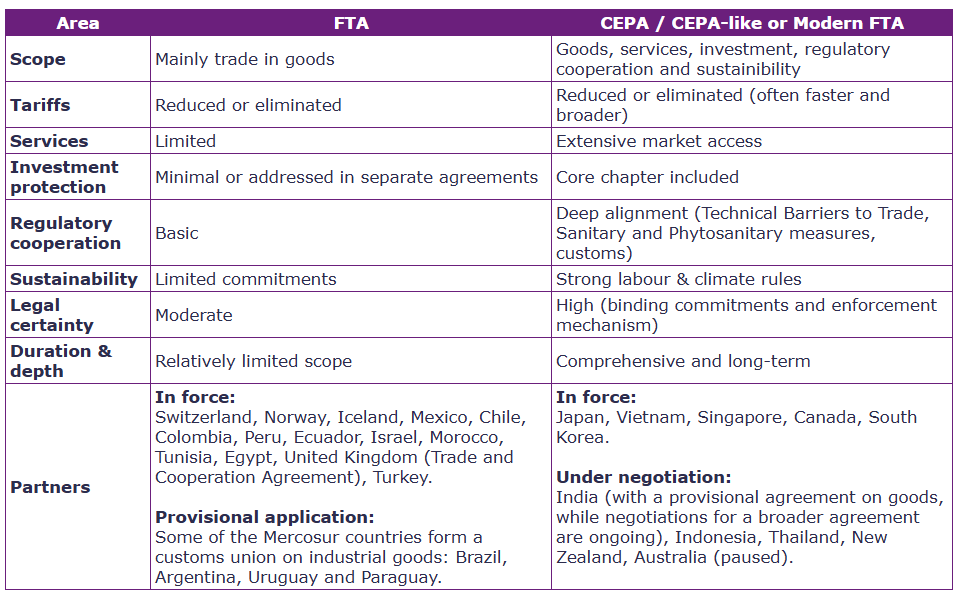

The European Union has concluded numerous free trade and economic partnership agreements over the past several decades in an attempt to diversify its markets, resources and ties around the world. Some are fully operational, such as the EU-Vietnam Free Trade Agreement (EVFTA), concluded in 2020. Others are still under negotiation, such as the Comprehensive and Enhanced Partnership Agreement (CEPA) with Indonesia, or the agreement with India (the FTA on goods is concluded; negotiations for a broader approach are still ongoing).

An EU CEPA generally goes beyond traditional FTAs. It establishes broader and more binding commitments, covering not only trade in goods but also services, investment protection, regulatory cooperation, and sustainability provisions.

Whether referred to as a CEPA or a “modern FTA”, these frameworks aim to anchor trade relations in predictable, stable, and transparent conditions of competition, underpinned by a long-term strategic perspective.

Negotiations with Indo-Pacific countries are gaining in momentum on these basis. The EU has concluded agreements with Japan, Vietnam, Singapore and South Korea, and is currently negotiating with India, Indonesia, Thailand, New Zealand, and Australia. While the scope of each agreement varies, they share a common objective: combining market openness with strict enforcement of trade, environmental and competition rules, particularly in carbon-intensive and strategically sensitive sectors such as stainless steel.

Implications for Stainless Steel

Stainless steel is frequently classified as a high-risk and potentially distortion-prone sector. This status reflects several structural factors:

- reliance on nickel and other strategic raw materials;

- capital-intensive production often supported by state intervention;

- exposure to global overcapacity;

- and increasing regulatory pressure linked to carbon emissions and sustainability standards.

The endemic volatility of nickel prices and geopolitical pressures regarding access to certain critical materials are exacerbating the sector’s structural imbalances.

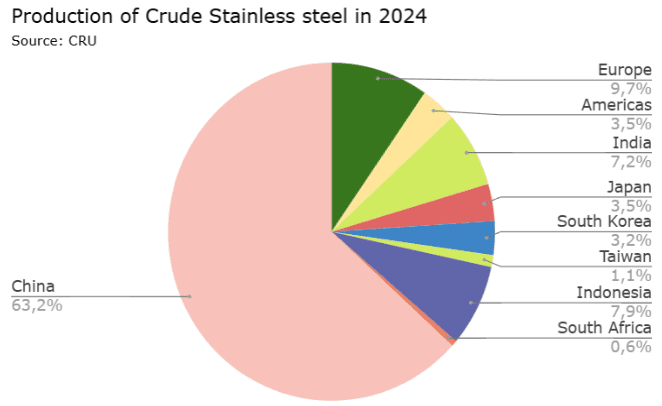

Furthermore, stainless steel production is highly concentrated: China accounts for more than 60% of global crude stainless steel production. Other Asian countries account for approximately 23% of the remainder. Competitive pressure is therefore particularly intense.

At the same time, the level of government intervention in some producing countries, particularly in Asia, can jeopardize those subject to market rules. Stainless steel flat products became and remain a central issue in EU trade agreements.

Following consultations with industry stakeholders, the European Commission has refined its analysis of the stainless steel supply chain. The trade risk assessment now incorporates policies relating to nickel and other critical raw materials, which are subject to structural price and supply volatility. The sector is thus considered within its overall value chain, rather than as a simple product category.

Moreover, the implementation of the Carbon Border Adjustment Mechanism (CBAM) and various European directives following the launch of the Green Deal, strengthens the control of carbon emissions from products entering the Union.

In this context, European agreements incorporate an open and rules-based trade approach, while maintaining robust safeguard mechanisms to protect production and sales against market distortions and environmental damage.

While tariffs are being progressively reduced, the agreements explicitly preserve each party’s right to use trade defense instruments in cases of dumping, unfair tariff and operational practices, or unjustified public subsidies. Tariff preferences apply and will continue to apply. However, trade defense measures remain in place to counter unfair practices and unjustified subsidies until market equilibrium is restored.

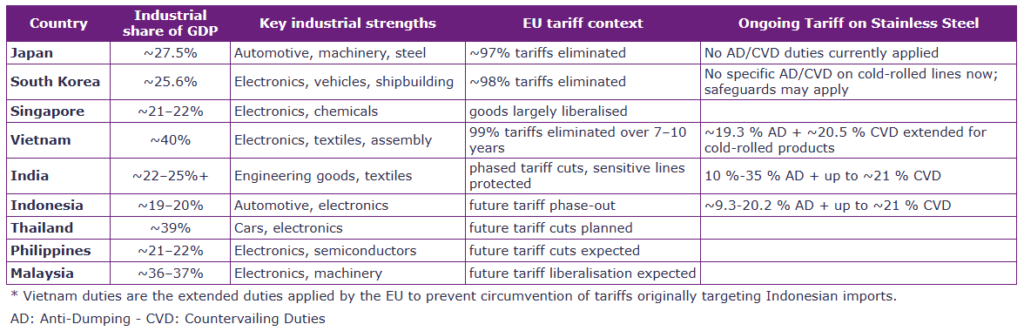

For example, flat-rolled stainless steel (HS codes 7219 and 7220) remains subject to several EU trade defence investigations. Vietnamese exports illustrate this dual framework: despite the EVFTA being in force, they face an anti-dumping duty of 19.3% and a countervailing duty of 20.5%. This case demonstrates the coexistence of tariff liberalisation and active trade defence enforcement.

Conclusion

The European Union has progressively expanded its trade network to strengthen rules-based exchanges and reduce reliance on volatile markets and geopolical disruptive contexts. Recent agreements aim to eliminate tariffs on nearly all goods, including industrial materials. EU agreements with Indo-Pacific partners establish a structured and predictable framework for trade cooperation. Beyond tariff reduction, they support regulatory convergence, sustainability standards and enhanced monitoring of market practices.

Within this framework, stainless steel is never fully liberalised. Tariff elimination coexists with permanent trade control instruments, including monitoring of prices, subsidies and overcapacity. As a result, the stainless steel sector operates in a more structured environment that links trade openness with sustainability and competitiveness requirements at both regional and global levels.

At Aperam, together with our industrial stakeholders, we contribute to a value chain that combines performance, regulatory compliance and responsible production standards.

Sources:

- https://policy.trade.ec.europa.eu/eu-trade-relationships-country-and-region/negotiations-and-agreements_en

- https://www.bundeswirtschaftsministerium.de/Redaktion/EN/Artikel/Foreign-Trade/ongoing-negotiations-for-free-trade-agreements-introduction.html

- https://policy.trade.ec.europa.eu/news/commission-fights-circumvention-tariffs-imports-cold-rolled-stainless-steel-2024-05-07_en

- https://eastasiaforum.org/2020/05/21/understanding-the-eu-vietnam-free-trade-agreement/

- https://www.kielinstitut.de/fileadmin/Dateiverwaltung/IfW-Publications/fis-import/82e3902e-610e-46e7-9176-83e37af0d5ab-KPB202.pdf

- https://www.crugroup.com/en/commodities/stainless-steel/